How the SEC Mutual Fund Rule Change Killed the 12b-1 Fee

For decades, the 12b-1 fee was a quiet line item in mutual fund expense ratios that most investors never noticed. Authorized by the SEC in 1980, it allowed funds to use shareholder assets to pay for marketing and distribution—essentially charging investors to be sold the product. By 2022, the fee had become a symbol of opaque fund costs, but its elimination through a regulatory overhaul went largely uncelebrated. The rule change was a significant shift in fund regulation, but its impact on investor costs is more nuanced than a simple victory for shareholders.

The Fee That Outlived Its Justification

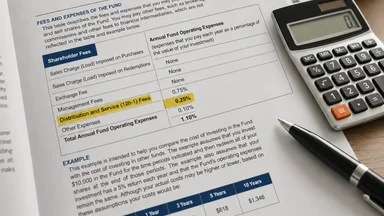

The 12b-1 fee was born in an era when mutual funds were sold through brokers and financial advisors who needed compensation for their time. The SEC's 1980 rule permitted funds to deduct up to 0.75% of assets annually for distribution costs, plus an additional 0.25% for shareholder service fees. At the time, this seemed reasonable: funds needed to grow assets under management to achieve economies of scale, and paying brokers a trailing commission helped keep the fund in front of clients.

But by the 2010s, the justification had worn thin. The rise of online brokerages and no-load funds meant investors could buy shares without a salesperson. Yet the 12b-1 fee persisted, buried in the prospectus and often mistaken for part of the management fee. Studies by the Securities and Exchange Commission and consumer advocates found that many investors had no idea they were paying for distribution—and that the fees added up to billions annually.

The fee structure also created a conflict of interest. Brokers had an incentive to recommend funds that paid higher 12b-1 fees, even if cheaper alternatives existed. The Department of Labor's fiduciary rule, proposed in 2016, aimed to address this, but it was vacated in court. The SEC's own Regulation Best Interest, adopted in 2019, required brokers to act in the client's best interest but did not ban 12b-1 fees outright.

By 2020, the fee was widely criticized as a relic of the paper era. The Investment Company Institute, a trade group, acknowledged that the fee's original purpose—covering the costs of printing and mailing prospectuses—had largely evaporated in the digital age. Still, the industry resisted change, arguing that the fee supported advisor services that investors valued.

The 2022 Rule Overhaul Nobody Celebrated

In November 2022, the SEC adopted amendments to Rule 12b-1 that effectively killed the fee for new share classes. The rule change required that any mutual fund share class created after the effective date could not impose a 12b-1 fee. Existing share classes with 12b-1 fees were grandfathered in, but funds had a transition period—until mid-2024—to either convert those shares to a non-12b-1 class or continue offering them under certain conditions.

The amendment was buried in a dense 200-page regulatory filing that also addressed swing pricing and hard close requirements for mutual funds. Mainstream financial press gave it modest coverage, largely because the SEC's press release framed it as a technical clarification rather than a dramatic shift. But for fund companies and broker-dealers, the implications were enormous: a core revenue stream was being phased out.

Why the muted reaction? Partly because the rule change did not ban 12b-1 fees retroactively. Funds could still collect them on existing shares, and many investors in older share classes continued paying the fee for years. The SEC estimated that investors would save roughly $3 billion annually once the transition was complete, but those savings would trickle in slowly.

Another reason for the quiet reception: the rule change was widely anticipated. The SEC had signaled its intent to revisit 12b-1 fees as early as 2018, and the industry had been preparing for a phaseout. Some fund families had already begun offering clean share classes—those without 12b-1 fees—well before the rule took effect. The 2022 amendments simply codified what was already becoming market practice.

Why the 12b-1 Fee Persisted for Decades

To understand why the 12b-1 fee lasted more than 40 years, you have to look at the economics of fund distribution. Broker-dealers relied on the fee as a trailing commission—a recurring payment that compensated them for ongoing advice and service. Without it, many brokers would have had to charge clients directly, a model that was unpopular and hard to implement. The fee was a convenient way to bundle compensation into the fund's expense ratio, making it invisible to the investor.

Fund families also used 12b-1 fees to pay for shelf space on brokerage platforms. Larger fund companies could negotiate lower fees, while smaller firms had to pay more to get their funds listed. This created a two-tier system where the cost of distribution was borne by shareholders, not by the fund company's profits. Critics called it a kickback; the industry called it a legitimate business expense.

Investors conflated 12b-1 fees with management fees, assuming that the total expense ratio was a single charge for portfolio management. In reality, the management fee covers the investment team's salaries and research costs, while the 12b-1 fee goes to the distributor. A typical fund with a 1.0% expense ratio might have 0.75% for management and 0.25% for 12b-1—meaning 25% of the fee was for marketing, not investing.

The industry lobbied hard to keep the fee, arguing that it supported the broker-advisor model and that eliminating it would reduce access to advice. Trade groups like the Investment Company Institute submitted comment letters to the SEC warning that a ban would harm small investors who relied on advisors. But the SEC ultimately concluded that the fee's costs—both financial and in terms of conflicted incentives—outweighed its benefits.

What Replaced the 12b-1 Revenue Stream

With the 12b-1 fee effectively banned for new share classes, fund companies and broker-dealers had to find new ways to cover distribution costs. The most common solution was the introduction of clean shares—mutual fund share classes that carry no 12b-1 fee and no sales load. Instead, brokers and advisors charge a separate advisory fee, typically a percentage of assets under management, which is disclosed on client statements.

This shift toward clean shares began before the 2022 rule change. In 2017, the SEC issued a no-action letter that allowed fund companies to offer clean shares on brokerage platforms, and several large fund families—including BlackRock, Vanguard, and Fidelity—launched clean share classes soon after. The 2022 rule simply accelerated the trend, making clean shares the default for new investors.

Another consequence was the acceleration of ETF adoption. Exchange-traded funds have never used 12b-1 fees; their expense ratios are typically lower than mutual funds', and they trade like stocks on exchanges. As mutual funds lost the ability to charge 12b-1 fees, the cost gap between mutual funds and ETFs narrowed, making ETFs even more attractive. By 2025, ETF assets under management had surpassed those of mutual funds in many categories.

Some fund companies raised their expense ratios to compensate for the lost 12b-1 revenue. For example, American Funds increased expense ratios on Class A shares by approximately 0.10% in 2023, citing the need to cover distribution costs previously paid through 12b-1 fees. This was especially common among smaller fund families that had relied heavily on the fee to cover marketing costs. In those cases, investors in older share classes may have seen their expense ratios rise, though the SEC's transition rules limited how much funds could increase fees without shareholder approval.

The Real Impact on Your Expense Ratio

For the average mutual fund investor, the elimination of 12b-1 fees meant a modest reduction in expense ratios. According to estimates from Morningstar, the average expense ratio for actively managed U.S. stock funds fell from roughly 0.65% in 2020 to about 0.48% in 2024, with the 12b-1 phaseout accounting for roughly 0.1 to 0.2 percentage points of that decline. For a $100,000 portfolio, that translates to annual savings of $100 to $200.

No-load funds—those that do not charge a sales commission—became more transparent. Previously, a no-load fund might still have a 12b-1 fee of up to 0.25%, which was confusing to investors. After the rule change, no-load funds essentially had to be clean shares, with no hidden distribution costs. This made it easier for investors to compare fund costs across different platforms.

However, the impact varied by channel. In the 401(k) market, revenue-sharing arrangements—where fund companies pay recordkeepers a portion of the expense ratio—remained common. These payments are not called 12b-1 fees, but they serve a similar purpose: covering the cost of plan administration. The SEC's rule change did not address revenue sharing in retirement plans, so some investors in 401(k)s may still be paying indirectly for distribution. This is a separate issue from the 12b-1 fee itself, but it highlights the broader challenge of hidden costs in fund distribution.

For small investors, the savings were real but not transformative. The elimination of the 12b-1 fee reduced the drag on returns, but for most people, the bigger factor remains the underlying management fee. A fund with a 0.50% expense ratio is still much more expensive than a comparable ETF with a 0.03% expense ratio. The 12b-1 fee was a relatively small piece of the cost puzzle.

A Contrarian Take: The Fee Was Never the Problem

It is tempting to celebrate the demise of the 12b-1 fee as a win for investors. But a closer look suggests that the fee was a symptom of a deeper problem: an opaque distribution system where costs are hidden from the end consumer. Eliminating the fee did not eliminate the conflicts of interest that arise when brokers are paid to recommend certain funds. It just shifted those payments to other forms.

Today, broker-dealers often receive revenue-sharing payments from fund companies in the form of "sub-transfer agency fees" or "shareholder servicing fees." These payments are not called 12b-1 fees, but they serve the same purpose: compensating the broker for selling the fund. The SEC's rule change did not ban these payments, and they remain largely invisible to investors. The difference is that they are now disclosed in a different line item in the prospectus.

Some industry observers argue that the real issue is not the fee structure but the sales culture itself. As long as brokers are paid more for selling one fund over another, conflicts will persist. The Department of Labor's fiduciary rule attempted to address this by requiring brokers to act in the client's best interest, but it was struck down in court. The SEC's Regulation Best Interest is a weaker substitute, and enforcement has been spotty.

Investor education remains the real gap. Most investors do not understand the difference between a load fund and a no-load fund, let alone the nuances of 12b-1 fees and revenue sharing. Regulation alone cannot cure a sales culture that thrives on complexity. The best protection is a knowledgeable investor who asks questions and compares costs. The 12b-1 fee was a small part of that picture—its elimination is a step forward, but not the end of the journey.

Case Study: The Vanguard Transition

To understand how a specific fund family handled the 12b-1 phaseout, consider Vanguard. The company had long been a proponent of low-cost investing and had already eliminated 12b-1 fees from most of its share classes before the SEC rule change. Vanguard's Admiral shares, for instance, have never carried a 12b-1 fee. However, the company did have some older share classes, such as Investor shares, that included a 0.25% 12b-1 fee in certain cases. In response to the 2022 rule, Vanguard converted most of those Investor shares to Admiral shares or other clean share classes, effectively eliminating the fee for existing shareholders. The transition was seamless for most investors, as Vanguard automatically converted shares without requiring action. This case illustrates that fund families with a low-cost culture were well-positioned for the rule change, while those that relied on 12b-1 fees faced more difficult adjustments.

In contrast, American Funds, which historically relied heavily on broker-sold share classes with 12b-1 fees, had to restructure its share class lineup. The company introduced new clean share classes and worked with broker-dealers to transition clients. Some investors experienced a temporary increase in expense ratios as the fund company adjusted its fee structure, but over time, the elimination of 12b-1 fees led to lower overall costs for new investors.

Practical Steps for Fund Investors

Investors who want to understand their fund costs can take several informational steps. First, reviewing the fund's prospectus for any line item labeled "service fee" or "distribution fee" can reveal whether a 12b-1 fee is still being charged. Even though 12b-1 fees are banned for new share classes, older share classes may still carry them. If a fund has a 12b-1 fee, investors may wish to explore whether a clean share class or institutional class is available, as these typically have lower expenses.

Second, clean shares or institutional classes are often the most cost-effective options for new purchases. Many brokerages now offer clean share classes as the default. For example, Vanguard's Admiral shares have no 12b-1 fee and low expense ratios, and Fidelity's ZERO funds have no expense ratio at all. Investors can compare the expense ratios of available share classes to identify the lowest-cost option.

Third, reviewing a brokerage's compensation structure can provide insight into potential conflicts. Some brokerages receive revenue-sharing payments from fund companies even after the 12b-1 phaseout. These payments are disclosed in the broker's Form CRS or fee schedule. Understanding whether an advisor charges a fee-only or commission-based model can help investors assess transparency.

Fourth, monitoring expense ratios after the transition period is prudent. Fund companies were allowed to convert existing share classes to new fee structures through mid-2024. Some funds may have raised their expense ratios to compensate for lost 12b-1 revenue. Checking account statements and comparing current expense ratios to those in 2022 can reveal any changes. If an expense ratio has increased, investors may contact the fund company for an explanation.

Finally, ETFs offer a simpler fee structure with typically lower expense ratios than mutual funds and no 12b-1 fees. They trade throughout the day, providing more control over execution. While some brokerages charge commissions for ETF trades, many now offer commission-free trading. For long-term investors, the cost savings from ETFs can be substantial, but individual circumstances vary.

This article is for informational purposes only and does not constitute personalized investment advice. Investors should consult a qualified financial professional before making any investment decisions.