SEC Reg BI Exemption That Legalized Revenue Sharing in Mutual Fund Share Classes

In June 2020, the U.S. Securities and Exchange Commission enacted Regulation Best Interest, a rule that replaced the old fiduciary standard for brokers and quietly reshaped how mutual fund firms get paid. While Reg BI was marketed as a consumer protection measure, a specific exemption it created effectively legalized revenue-sharing arrangements that had previously existed in a regulatory gray zone. Today, these arrangements allow fund families to pay brokers for steering clients into higher-fee share classes, generating billions in annual revenue for the brokerage industry at the expense of investor returns. This article explains the rule, its downstream effects, and what investors can do about it.

The Rule That Quietly Changed How Fund Firms Get Paid

Reg BI took effect on June 30, 2020, after years of debate following the 2008 financial crisis. Its stated purpose was to raise the standard of conduct for brokers when making investment recommendations to retail clients. The rule requires brokers to act in the "best interest" of the client, but it does not impose a uniform fiduciary duty. Instead, it created a four-part framework: disclosure, care, conflict of interest, and compliance obligations.

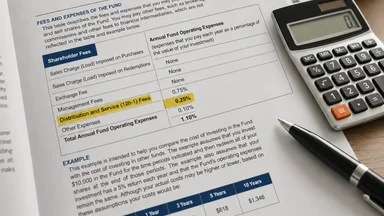

The critical exemption lies in the care obligation. Under Reg BI, brokers are not required to recommend the lowest-cost share class available. They must merely have a "reasonable basis" to believe the recommendation is in the client's best interest. This opened the door for brokers to recommend mutual fund share classes that carry 12b-1 fees—ongoing distribution fees that fund families pay to broker-dealers for selling their funds. These fees, typically ranging from 0.25% to 1.00% annually, are passed on to investors as higher expense ratios.

Revenue-sharing arrangements are not new. Before Reg BI, some brokers received payments from fund families under the "shelf space" model, but the legal footing was murky. Reg BI effectively legitimized these payments by allowing them as long as the broker discloses the conflict in a vague, boilerplate document. The SEC's own estimates suggested that Reg BI would not reduce revenue-sharing; it would merely make it more transparent. However, a 2024 FINRA report titled "Review of Revenue-Sharing Practices in Broker-Dealer Mutual Fund Sales" found that roughly 70% of broker-sold mutual funds still use revenue-sharing, and disclosure documents often bury the details in fine print.

Fund families now design share classes specifically for broker distribution, with higher expense ratios that include revenue-sharing payments. For example, Class A shares might carry a front-end load and a 12b-1 fee, while Class C shares have higher ongoing fees. Clean shares—which strip out 12b-1 fees and are sold at net asset value—exist but are rarely offered to retail clients through full-service brokers. The result is a system where share class selection is driven by revenue potential, not cost efficiency for the investor.

What Reg BI Actually Permitted That Prior Rules Did Not

Before Reg BI, the standard for brokers was "suitability"—a lower bar that only required recommending products appropriate for the client's risk tolerance and investment objectives. Revenue-sharing was technically allowed but faced scrutiny from regulators like FINRA, which occasionally fined firms for excessive fees. The 2010 Dodd-Frank Act directed the SEC to study a uniform fiduciary standard, but the agency dragged its feet for a decade.

Reg BI explicitly permitted brokers to receive third-party payments from fund families as long as the broker discloses the conflict. The rule does not require brokers to disclose the dollar amount of revenue they receive from a specific fund family. Instead, they can provide a generic summary of "material conflicts of interest." This lack of dollar-level disclosure makes it nearly impossible for investors to know how much their broker is being paid to recommend a particular fund.

Another key provision: Reg BI exempted "clean shares" from its disclosure requirements. Clean shares are mutual fund shares that do not carry 12b-1 fees or other distribution charges. The rule treats them as a baseline, but brokers are not required to recommend them. In practice, this means a broker can recommend a higher-fee share class and simply note that a lower-cost option exists. The care obligation only requires the broker to have a reasonable basis that the recommendation is in the client's best interest, which can be justified by vague factors like "access to the broker's advice" or "additional services."

The result is a tilt toward higher-fee share classes. A 2023 study by the University of Chicago's Booth School of Business found that broker-sold mutual funds charge expense ratios roughly 0.50% higher than identical funds sold directly to investors. This gap is almost entirely attributable to 12b-1 fees and revenue-sharing payments. The study estimated that these fees cost investors roughly $5 billion annually in excess fees, a figure that aligns with a 2022 Wharton School analysis.

The Downstream Effect on Investor Costs and Returns

The math on revenue-sharing is straightforward but damaging. Consider a $10,000 investment in a mutual fund with a 0.75% expense ratio versus a clean share class with a 0.25% expense ratio. Over ten years, assuming a 6% annual return, the higher-fee fund would cost the investor roughly $600 more in cumulative fees. For a retirement account with $100,000, the difference balloons to over $6,000. These fees compound, reducing the final portfolio value significantly.

Smaller accounts are disproportionately affected. Investors with $5,000 to $50,000 are often steered into Class A or C shares because those share classes generate higher commissions for brokers. Institutional share classes, which have the lowest fees, are reserved for accounts over $1 million. A 2024 SEC examination of a major broker-dealer found that 80% of retail accounts under $50,000 were invested in share classes with 12b-1 fees, even when clean shares were available for the same fund.

The rise of exchange-traded funds has put additional pressure on mutual fund share classes. ETFs typically have expense ratios below 0.10% and no 12b-1 fees. Yet many brokers continue to recommend mutual funds, partly because ETFs do not generate revenue-sharing payments. A 2025 FINRA investor alert titled "Understanding Mutual Fund Share Classes and Costs" noted that some brokers receive "revenue-sharing payments that can be 10 times higher for mutual funds than for ETFs." This creates a misaligned incentive that hurts investors.

Fee compression in the asset management industry has made the problem worse. As index funds and ETFs push down costs, fund families have turned to revenue-sharing as a way to maintain profit margins. The average expense ratio for actively managed mutual funds has declined only slightly, from 1.10% in 2010 to roughly 0.90% in 2025, but the share of that fee going to broker-dealers has increased. According to Morningstar, 12b-1 fees now account for roughly 40% of total fund expenses in broker-sold share classes.

Why the Industry Defends Revenue Sharing as Legal

The brokerage industry argues that revenue-sharing is a legitimate way to compensate brokers for providing advice and services. The Securities Industry and Financial Markets Association, a trade group, has stated that Reg BI's "best interest" standard is sufficient to protect investors, and that additional restrictions would reduce access to advice for small investors. They claim that clean shares are available but that many investors value the advice that comes with higher-fee share classes.

Critics counter that the "best interest" standard is too vague. Reg BI does not define what constitutes a client's best interest, leaving it to firms to interpret. In practice, this means that brokers can justify recommending a higher-fee share class by pointing to services like quarterly statements or phone support—services that are often available with lower-cost options. The SEC has brought only a handful of enforcement actions under Reg BI, mostly for egregious violations like outright fraud.

Industry lobbying has been effective at blocking tighter rules. In 2022, the SEC proposed a rule that would have required brokers to disclose the dollar amount of revenue-sharing payments, but the proposal stalled after intense pushback from the brokerage industry. The Investment Adviser Association argued that the rule would impose "significant compliance costs" without clear benefits. The proposal was shelved and has not been resurrected.

Another defense is that revenue-sharing is not unique to mutual funds. Insurance companies, annuity providers, and even some ETF sponsors have similar arrangements. The industry argues that singling out mutual funds would create an uneven playing field. However, mutual funds remain the largest pool of retail investment assets, and the impact of revenue-sharing is most concentrated in that market. As of late 2024, mutual funds held roughly $20 trillion in assets, with about half in broker-sold share classes.

Evidence from Recent Regulatory Filings and Studies

Regulatory filings and academic studies provide a clear picture of the problem. A 2024 FINRA report examined 50 large broker-dealers and found that 70% of mutual fund sales involved revenue-sharing arrangements. The report also noted that disclosure documents were often "lengthy and confusing," with the average Form CRS (Client Relationship Summary) exceeding 10 pages. FINRA has since issued guidance urging firms to simplify disclosures, but compliance remains voluntary.

SEC examination findings have been damning. In a 2023 sweep, SEC examiners found that 40% of broker-dealers failed to properly disclose revenue-sharing conflicts. Some firms provided clients with generic brochures that did not mention specific payments. The SEC issued deficiency letters but did not levy fines in most cases. A 2025 enforcement action against a large brokerage resulted in a $10 million settlement for recommending higher-fee share classes to thousands of clients without adequate disclosure.

Academic research quantifies the cost. A 2022 Wharton School study estimated that revenue-sharing costs U.S. investors roughly $5 billion annually in excess fees. The study used data from 2015 to 2020, before Reg BI took effect, suggesting the problem has likely grown. A separate 2024 study by the University of California, Berkeley found that investors in broker-sold funds underperform those in direct-sold funds by roughly 1% per year, after controlling for risk and expenses.

State-level actions have highlighted the issue. In 2023, the state of Massachusetts sued a major brokerage firm, alleging that it had violated state fiduciary laws by recommending higher-fee share classes. The firm settled for $8 million in 2024, agreeing to restitution but not admitting wrongdoing. The case set a precedent for state regulators to step in where the SEC has not. California's Department of Financial Protection and Innovation is reportedly investigating similar practices.

Practical Steps for Investors to Avoid Hidden Fees

Investors can take concrete steps to avoid the hidden costs of revenue-sharing. First, request only clean shares or institutional share classes when buying mutual funds. Clean shares have no 12b-1 fees and are available at net asset value. Not all brokers offer them, but asking explicitly can force the issue. If your broker cannot provide clean shares, consider moving your account to a fee-only advisor who charges a flat fee or a percentage of assets under management, not commissions.

Second, compare expense ratios across share classes for the same fund. A fund's prospectus lists all available share classes, usually labeled A, C, I, etc. The expense ratio for Class I (institutional) shares is often half that of Class A shares. If you have less than $1 million, you may not qualify for institutional shares, but many fund families will waive the minimum if you ask. Third, prefer ETFs over mutual funds in taxable accounts. ETFs generally have lower expense ratios and no 12b-1 fees. They also offer tax advantages because of their in-kind creation and redemption process.

Fourth, ask your broker for a written disclosure of any third-party payments they receive from fund families. Under Reg BI, brokers must disclose conflicts, but they are not required to provide dollar amounts. However, you can request a breakdown of revenue-sharing payments for your specific holdings. If your broker refuses, consider that a red flag. Fifth, use online tools like Morningstar's Mutual Fund Fee Analyzer to compare costs across funds and share classes.

Finally, consider working with a fiduciary advisor who is held to a higher standard. Registered investment advisers are bound by the Investment Advisers Act of 1940, which imposes a fiduciary duty to act in the client's best interest. Unlike brokers, RIAs cannot accept revenue-sharing payments without disclosing them and obtaining client consent. Many RIAs charge a flat fee or a percentage of assets, aligning their incentives with yours. For more on broker payment disclosures, see our article on SEC Rule 606(a).

What Regulatory Reform Could Change Next

The regulatory landscape is shifting, but change is slow. The SEC is reportedly considering a rule that would ban revenue-sharing in retirement accounts, similar to the Department of Labor's fiduciary rule that was struck down in 2018. A draft proposal circulating in early 2025 would require brokers to recommend only the lowest-cost share class in IRA accounts. However, industry pushback is expected to delay any final rule until 2027 or later.

The DOL is also working on expanding its fiduciary rule to cover IRAs. The current DOL rule, which took effect in 2024, applies only to rollover recommendations from employer-sponsored plans like 401(k)s. Expanding it to IRAs would require brokers to act as fiduciaries when recommending investments in retirement accounts, effectively banning revenue-sharing in those accounts. The DOL is expected to propose an expansion in late 2026, but legal challenges are likely.

On the legislative front, a bipartisan bill introduced in the House in 2025 would mandate dollar-level disclosure of revenue-sharing payments. The bill, called the "Fee Transparency for Investors Act," would require brokers to provide clients with an annual statement showing exactly how much each fund family paid the broker. The bill has support from consumer advocacy groups but faces opposition from the brokerage industry, which argues it would confuse investors. The bill's future is uncertain.

State-level actions may accelerate change. California's financial regulator is considering a rule that would require brokers to recommend the lowest-cost share class available, regardless of revenue-sharing. If enacted, the rule could set a precedent for other states. Meanwhile, a class-action lawsuit filed in 2024 against several large brokerages is moving forward, alleging that revenue-sharing violates state fiduciary laws. The outcome could force firms to change their practices nationwide.

The path to reform is uncertain, but the pressure is mounting. As investors become more aware of hidden fees, they are voting with their feet. Assets in clean shares and ETFs have grown steadily, and fee-only advisors are gaining market share. Whether through regulation or market forces, the era of hidden revenue-sharing may be coming to an end.

Disclaimer: This article is for informational and educational purposes only and does not constitute personalized investment, legal, or tax advice. Consult a qualified professional for advice tailored to your specific financial situation.