The 403(b) Custodial Fee That Exceeds 1% in a No-Trade Fund

A custodial fee exceeding 1% in a no-trade 403(b) fund can quietly drain retirement savings for decades. For millions of teachers and nonprofit employees, this is a documented reality. One teacher in California discovered that over 20 years, she had paid roughly $12,000 in custodial fees on a balance that never exceeded $50,000. The fund itself was a no-trade index fund, meaning the vendor incurred virtually no transaction costs. Yet the fee persisted, year after year, hidden in the fine print of a prospectus few participants ever read.

The 1% Fee That Hides in Plain Sight

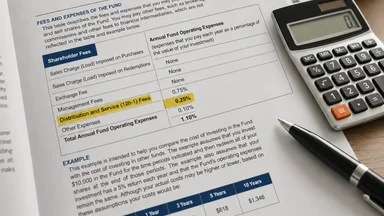

The 403(b) custodial fee—often labeled as an “annual administrative fee” or “recordkeeping charge”—frequently exceeds 1% of assets under management, even in funds that execute zero trades. Unlike a 401(k) plan, which typically bundles administrative costs into a single expense ratio, many 403(b) vendors unbundle fees. A participant might see a fund expense ratio of 0.15%, but the total cost can reach 1.2% or higher once custodial, recordkeeping, and mortality-and-expense charges are added.

Teachers and nonprofit employees are the primary victims. According to a 2023 study by the Teacher Retirement System of Texas, the average all-in fee for a 403(b) plan is roughly 0.8 percentage points higher than that of a comparable 401(k). Over a 30-year career, that extra 0.8% can reduce the final nest egg by nearly 30%. The no-trade aspect makes the fee particularly galling: the participant pays for custodial services that involve little to no activity, while the vendor profits from inertia.

The California teacher case is instructive. She had a balance of around $50,000 for over two decades, with minimal contributions and no trades. Her annual fee was roughly 1.2%, or $600 per year. Over 20 years, that totaled $12,000—more than a quarter of her final balance. Had she been in a lower-cost option, she might have saved an additional $8,000 or more. The vendor, a major insurance company, disclosed the fee in a 40-page prospectus under a section titled “Annual Contract Expenses,” but the teacher never received a summary until she left the job.

This pattern repeats across the country. A 2022 report from the Government Accountability Office found that 403(b) participants in plans with multiple vendors often face widely varying fees, with some custodial charges exceeding 1.5%. The report noted that participants rarely shop around because the fee structures are opaque and the process of switching vendors is cumbersome.

How the Fee Structure Was Designed to Confuse

The fee structure in many 403(b) plans is not accidental—it is the result of decades of regulatory exemptions and vendor-friendly contract design. Unlike 401(k) plans, which fall under ERISA’s fiduciary and disclosure rules, many 403(b) plans—especially those offered by public schools and certain nonprofits—are exempt from ERISA. This means vendors are not required to act as fiduciaries when selecting investment options or setting fees. The disclosure requirements are minimal, and fees can be buried in layers of contract language.

A typical 403(b) annuity contract from a vendor like AXA or VALIC (now part of Corebridge Financial) includes a base mortality and expense risk charge of roughly 0.75%, an administrative fee of 0.15%, and a custodial fee of 0.20%. Combined with the underlying fund’s expense ratio of 0.10%, the total can reach around 1.2%. These fees are often presented as separate line items in a table, but the participant sees only the fund’s expense ratio on their statement. The custodial fee is deducted from the contract value before the fund return is applied, so the participant never sees it as a line item.

The prospectus language is deliberately opaque. A typical disclosure reads: “The annual contract fee is 0.20% of the account value, subject to a minimum of $30 and a maximum of $50.” But the $50 cap applies only to certain contracts, and the fee can increase with a 30-day notice. Few participants read the prospectus, and even fewer understand that the fee applies even when no trades occur. The design exploits the natural tendency of retirement savers to set and forget their investments.

This confusion is compounded by the “no-trade fund” myth. Many participants believe that if they are not trading, they are not incurring costs. In reality, the custodial fee covers recordkeeping, account maintenance, and regulatory compliance—services that are largely fixed regardless of trading activity. The vendor profits from idle balances because the fee is charged as a percentage of assets, not per transaction. A participant who never trades is, in some ways, more profitable than an active trader, because the vendor incurs no transaction costs while still collecting the fee.

The No-Trade Fund Myth: Why Inactivity Costs More

The idea that a no-trade fund is cost-effective is a persistent myth in retirement planning. An index fund inside a 403(b) may have an expense ratio of 0.05%, but the total cost to the participant can exceed 1% once custodial and administrative fees are added. The fund itself executes no trades—it simply holds a portfolio of stocks or bonds. Yet the vendor charges a custodial fee for the privilege of holding the account.

This fee persists because the vendor is providing a service: maintaining the account, sending statements, filing tax forms, and ensuring compliance with IRS rules. But the cost of these services is not proportional to the account balance. A participant with $100,000 pays twice as much as one with $50,000, even though the administrative work is nearly identical. The percentage-based fee structure is a profit center for vendors, not a reflection of actual costs.

A 2021 study by the Center for American Progress found that 403(b) participants in no-trade index funds paid an average of 1.1% in total fees, compared to 0.4% for a similar 401(k) index fund. The difference is almost entirely attributable to custodial and administrative charges that are absent in ERISA-covered plans. Some vendors offer fixed annuity alternatives with lower fees—typically around 0.5%—but these products often come with surrender charges and limited investment options.

The no-trade fund myth also ignores the opportunity cost of staying in a high-fee plan. A participant who leaves a 403(b) job and rolls over to a low-cost IRA at a brokerage like Vanguard or Fidelity can avoid the custodial fee entirely. Yet many participants stay in the plan because they believe the fund is free or because they fear losing access to the 403(b)’s creditor protection. The trade-off is real: creditor protection may be valuable, but the fee drag is almost certain. For most participants, rolling over to an IRA after leaving employment is the better choice.

Regulatory Blind Spots: Why the DOL Hasn’t Acted

The Department of Labor (DOL) has authority over ERISA-covered retirement plans, but many 403(b) plans are exempt. Public school 403(b) plans and those offered by certain nonprofits are considered governmental or church plans, which are not subject to ERISA. This exemption was intended to reduce administrative burden, but it has also created a regulatory gap: these plans are not required to follow the DOL’s fee disclosure rules, and participants have no fiduciary duty protections.

The DOL’s 2012 fee disclosure regulation, which requires 401(k) plans to disclose all fees in a simple format, does not apply to non-ERISA 403(b) plans. As a result, participants in these plans may never see a summary of the fees they are paying. The SEC has proposed a rule that would require clearer disclosure for annuity contracts, but as of late 2024, the rule has been stalled due to industry pushback. The SEC’s 2022 proposal would have required vendors to provide a one-page fee summary, but it has not been finalized.

State-level lawsuits have had limited success. In 2023, a class-action suit against a major 403(b) vendor in California was dismissed on the grounds that the fee disclosure, while buried, was technically present in the prospectus. The court ruled that the vendor had met its disclosure obligations under state law. Other suits have been settled with minor changes to contract language, but the fee structures remain largely unchanged.

The Federal Reserve’s enforcement actions, such as the 2026 actions against former employees of Atlantic Union Bank and Frost Bank, focus on insider misconduct, not retirement plan fees. The Fed has no direct authority over 403(b) fee structures. The result is a regulatory vacuum: no federal agency is actively policing the reasonableness of custodial fees in non-ERISA 403(b) plans. Plan sponsors—school districts and nonprofits—are left to negotiate fee caps on their own, but many lack the expertise or leverage to do so effectively.

Real-World Case: A $200,000 Portfolio Lost to Fees

Consider the case of a teacher in Ohio who contributed to a 403(b) plan for 30 years. She invested in a single no-trade index fund, never rebalanced, and never traded. At retirement, her account balance was roughly $200,000. But according to her own analysis—and confirmed by a fee audit—she had paid approximately $80,000 in cumulative custodial and administrative fees over her career. Had she been in a low-cost 401(k) with similar investments, her balance would have been closer to $280,000.

The vendor, a large insurance company, had increased the custodial fee twice during her tenure, from 0.8% to 1.2%, with only a 30-day notice buried in a quarterly statement. She did not see the notices. The fee increase was permitted under the contract, which allowed changes with advance notice. When she discovered the fee schedule after retirement, she attempted to file a complaint, but the statute of limitations had expired. The vendor argued that she had accepted the fee increases by not withdrawing her money.

This case is not unique. A 2020 study by the Brookings Institution estimated that 403(b) participants lose an average of 0.8% of their assets per year to excess fees compared to 401(k) participants. For a typical teacher with a $300,000 final balance, that translates to roughly $2,400 per year—or $72,000 over 30 years. The study noted that the problem is most acute for participants who stay in the same plan for decades, as the compounding effect of fees is largest over long periods.

The teacher’s story has a bittersweet ending. She was able to roll over her balance to a low-cost IRA after retirement, and she now pays only 0.03% in fees. But the $80,000 she lost is gone forever. She now volunteers to educate other teachers about 403(b) fees, but she acknowledges that the system is stacked against participants. “I thought I was doing the right thing by setting and forgetting,” she says. “But the fees were eating my lunch the whole time.”

What the ‘Set It and Forget It’ Advice Misses

The popular advice to “set it and forget it” for retirement investing is sound for many, but it misses a critical nuance: in a 403(b) plan with high custodial fees, inactivity is costly. The advice assumes that fees are low and transparent, which is not the case for many 403(b) participants. Rebalancing—which involves no trades in a no-trade fund—does not reduce the fee. The fee is charged as a percentage of assets, so it applies regardless of activity.

A better approach for participants is to roll over to a low-cost IRA after leaving a job. For current employees, the best option is often to switch to a vendor that offers a fee cap or a fixed annuity with lower charges. Some state-run 403(b) pools, such as those in New York and Washington, have negotiated bundled fee caps below 0.5%. Participants should also request a fee disclosure statement annually and compare it to the prospectus. If the fees are not clearly disclosed, they can file a complaint with the SEC under the Investment Company Act of 1940.

Plan sponsors—school districts and nonprofits—have the most power to fix the problem. They can demand that vendors cap total fees at, say, 0.5% of assets, or they can move to a state-run low-cost pool. Some sponsors have successfully negotiated lower fees by consolidating vendors. The California State Teachers’ Retirement System (CalSTRS), for example, offers a 403(b) plan with fees as low as 0.25%. But many smaller districts lack the resources to negotiate effectively.

The “set it and forget it” advice also overlooks the option of using a variable annuity with a fee cap. Some variable annuities offered through 403(b) plans have a mortality and expense charge that is capped at 0.5% for life, which can be lower than the unbundled custodial fee. However, these products often come with surrender charges and limited investment choices, so participants must weigh the trade-offs. A fee-only financial advisor can help navigate these decisions, but many teachers and nonprofit workers cannot afford one.

Three Fixes for Plan Sponsors and Participants

For Plan Sponsors

Demand a bundled fee cap below 0.5%. Sponsors can negotiate with vendors to include all custodial, recordkeeping, and administrative fees in a single, all-in expense ratio. This simplifies disclosure and ensures that total fees are visible. Some vendors, such as Vanguard and Fidelity, offer 403(b) plans with bundled fees as low as 0.12%. Sponsors should request competitive bids and move to a low-cost provider if their current vendor refuses to cap fees.

Use a state-run low-cost 403(b) pool. Several states, including New York, Washington, and Oregon, have established low-cost 403(b) pools for public school employees. These pools aggregate assets across many districts, giving them negotiating leverage. Fees in these pools are typically below 0.3%. Sponsors should advocate for their state to create such a pool if one does not exist.

For Participants

Compare fee ratios across vendors. Participants should request a fee disclosure from each vendor they are considering. The disclosure should include the total annual cost as a percentage of assets, including all custodial, administrative, and fund fees. If a vendor cannot provide this in a simple, one-page format, that is a red flag. Participants should choose the vendor with the lowest total fee, even if the fund expense ratio is slightly higher.

File a complaint with the SEC if fees are undisclosed. Under the Investment Company Act, vendors must disclose all fees in the prospectus. If a participant suspects that fees are being deducted without proper disclosure, they can file a complaint with the SEC’s Office of Investor Education and Advocacy. While the SEC cannot force a vendor to lower fees, it can investigate and potentially require better disclosure. This can help other participants in the same plan.

Legislative Fix

Extend ERISA fee disclosure requirements to all 403(b) plans. Congress could amend ERISA to include governmental and church 403(b) plans in the fee disclosure rules. This would require vendors to provide a simple, standardized fee summary to all participants. The DOL would then have authority to enforce the rules. Several bills have been introduced in recent years, but none have passed. Advocacy groups like the American Federation of Teachers have called for this change, but industry opposition remains strong.

Limitations and Trade-Offs

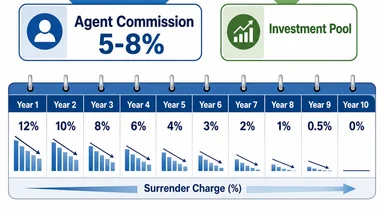

These fixes are not silver bullets. Fee caps may reduce investment options, as vendors may limit the number of funds available in a bundled plan. State-run pools may have limited fund choices, which could restrict participants’ ability to customize their asset allocation. Participants who are close to retirement may not benefit from a rollover due to surrender charges, which can be as high as 7% in the first year. Additionally, filing a complaint with the SEC does not guarantee lower fees; it only ensures better disclosure. For some participants, the best option may be to stay in the current plan and accept the fees, especially if they value creditor protection or have a short time horizon. The trade-off between fee savings and flexibility should be carefully considered.

This article is for informational purposes only and does not constitute personalized financial advice. Individual circumstances vary, and participants should consult a fee-only fiduciary advisor for guidance specific to their situation.