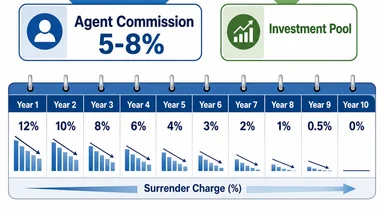

The Annuity Surrender Schedule That Compensates the Agent at Year One

When you buy an annuity, the agent typically earns a commission equal to 5–8% of your premium in the first year. That money comes from the insurance company, but the company recoups it through a deferred sales charge — the surrender schedule — that can cost you 10–12% of your account value if you withdraw in year one. Understanding who gets paid, when, and from what pocket is essential before signing the application.

The First-Year Commission Bump: How Front-Loaded Fees Work

Insurance agents selling annuities are compensated primarily through commissions, not hourly fees. For a typical fixed indexed or variable annuity, the agent receives a lump sum equal to roughly 5–8% of the premium at the time of sale. This is called a front-loaded commission. The carrier deducts this amount from the premium before investing the remainder.

To recoup that upfront payout, the insurer builds a surrender charge schedule into the contract. In year one, the surrender charge is usually 10–12% of the amount withdrawn above any free-withdrawal allowance. The charge declines by roughly 1% per year over a period of 7–10 years, after which it reaches zero. The schedule is designed so that the total surrender charges collected over the early years roughly equal the commission paid to the agent.

Internal Revenue Code section 1035 allows tax-free exchanges of one annuity for another, but the new contract typically starts a fresh surrender schedule. This means that swapping policies can reset the lock-in period, effectively extending the time during which the carrier recoups its costs.

Some states require insurers to disclose the commission amount in the contract or in a separate illustration. However, the disclosure may be buried in fine print. A 2024 study by the National Association of Insurance Commissioners found that fewer than half of annuity buyers recalled being told the commission amount at the time of sale.

Follow the Money: Who Gets Paid and When

The agent's commission is only one piece of the fee stack. The insurance company also deducts a mortality and expense risk charge (M&E) that typically runs 1.25–1.50% of the account value annually. This covers the insurer's risk that the annuitant lives longer than expected and the cost of administering the contract. Administrative fees add another 0.15–0.30% per year.

For variable annuities, the underlying investment options — subaccounts — charge their own fees, often 0.5–1.5% annually. These are in addition to the M&E and admin fees. The total annual cost of a variable annuity can reach 2.2% or more, according to a Morningstar study from late 2024. That study found that the average variable annuity had total annual expenses of 2.2%, with the highest-cost products exceeding 3.5%.

Fixed indexed annuities generally have lower annual fees, often around 1% or less, but they cap the upside you can earn from market index gains. The surrender charge structure is similar, though some fixed indexed products have no explicit annual fee — the costs are embedded in the crediting rate formula.

The surrender charge itself is not an annual fee; it is a one-time penalty triggered only upon withdrawal. But because the charge is highest in the early years, it effectively locks the buyer into the contract. The carrier uses the surrender charge revenue to recover the commission and other acquisition costs.

The Surrender Schedule as a Lock-In Mechanism

The typical surrender period runs 7–10 years. In year one, the surrender loss — the difference between account value and cash value — is roughly equal to the total first-year commission. For a $100,000 premium, a 10% surrender charge means you would receive $90,000 if you withdrew immediately, while the agent earned $5,000–$8,000. The insurer keeps the difference to cover its costs.

The break-even point — when the cumulative surrender charges no longer exceed the commissions paid — usually occurs around year 5 to 7, depending on the schedule. After that, the carrier has recouped its upfront outlay, and the surrender charge continues to decline until it reaches zero.

Some contracts include a market value adjustment (MVA) that can increase the loss if interest rates have risen since purchase. The MVA reflects the change in the value of the underlying bonds that back the annuity. In a rising-rate environment, the MVA can add several percentage points to the surrender penalty.

Internal Revenue Code section 72(q) imposes an additional 10% penalty on early withdrawals before age 59½, applied to the gain portion of the distribution. This penalty is separate from the surrender charge and can make early access extremely costly. For example, a $100,000 annuity with $20,000 of gain withdrawn at age 50 could trigger a $2,000 IRS penalty on top of the surrender charge.

Comparing Annuity Fee Loads Across Product Types

Not all annuities have the same fee structure. Fixed indexed annuities often have surrender charges in the 0–3% range for shorter-duration contracts, though some can go higher. Annual fees are typically around 1% or less, embedded in the crediting rate. Variable annuities carry higher annual expenses — 1–2% for the M&E and admin, plus 0.5–1.5% for subaccount fees — and surrender charges that start at 7–10% and decline over 7–10 years.

Immediate annuities, which begin payments right away, generally have no surrender charge because there is no account value to withdraw. However, the payments are irrevocable; you cannot access a lump sum once the contract is annuitized. This makes them unsuitable for anyone who might need liquidity.

Fee-only advisors, who charge a percentage of assets under management (AUM) rather than commissions, typically recommend low-cost annuity alternatives or no-load annuities. A 1% AUM fee on a $100,000 portfolio costs $1,000 per year, compared to a 5–8% upfront commission on a commissioned annuity. Over 10 years, the AUM fee totals about $10,000 (assuming no growth), while the commission is paid once. However, the AUM fee is ongoing, while the surrender charge eventually expires.

A Morningstar study from 2024 found that the average variable annuity had total annual costs of 2.2%, including all layers. The study noted that low-cost variable annuities with total expenses under 1.5% are available but represent a small share of the market.

Tax Treatment of Early Withdrawals: LIFO and the Gain-First Rule

Annuity withdrawals are taxed under a last-in, first-out (LIFO) method. This means that any gain in the contract is deemed to come out first, before your principal. The gain portion is taxed as ordinary income, which can be as high as 37% at the federal level for high earners in 2025. State income taxes add 0–13.3% depending on your state of residence.

For example, if you have a $100,000 annuity with $20,000 of gain and you withdraw $10,000, the entire $10,000 is treated as gain and taxed at your ordinary income rate. You do not get any tax-free return of principal until all gain has been withdrawn. This rule applies to non-qualified annuities (purchased with after-tax dollars). Qualified annuities (held in an IRA or 401(k)) are taxed entirely as ordinary income upon withdrawal.

A section 1035 exchange defers taxation but resets the surrender clock. If you exchange one annuity for another, you do not pay tax on the gain at that time, but the new contract's surrender schedule starts from year one. This can be a trap for those who switch policies frequently.

Partial surrenders from contracts without separate accounts may be subject to a pro-rata gain rule under certain interpretations, but most modern annuities use the LIFO method. Always check the contract language. The IRS has issued guidance in Revenue Ruling 2005-36 confirming that non-qualified annuities generally follow LIFO.

When the Surrender Schedule Benefits the Buyer

Despite the costs, surrender schedules can benefit buyers who hold the contract for the long term. If you keep the annuity for 10 years or more, the surrender charge expires entirely, and you can withdraw without penalty (though taxes still apply). The insurance company's costs are already recouped, so the ongoing fees may be lower than comparable investment products.

Some annuities offer guaranteed lifetime withdrawal benefit (GLWB) riders that promise a steady income stream regardless of market performance. These riders add cost — typically 0.5–1.0% annually — but can be valuable for retirees who want income certainty. The surrender charge ensures that the insurer can afford to offer these guarantees.

Fixed annuities often credit interest at rates that exceed bank CDs, especially in a rising-rate environment. As of mid-2025, some multi-year guaranteed annuities (MYGAs) offered crediting rates around 4–5%, compared to 2–3% for CDs. The trade-off is the surrender charge and lack of FDIC insurance.

Tax deferral is another benefit. Unlike a taxable brokerage account, you do not pay annual taxes on interest or capital gains inside the annuity. This allows the account to compound without the drag of annual taxation. For someone in a high tax bracket, this can be a meaningful advantage over 20–30 years.

In some states, annuities can be used in Medicaid spend-down planning to shelter assets while still generating income. The rules vary by state and are complex, but an annuity that meets certain requirements may be excluded from countable assets. This is a niche benefit that requires careful legal advice.

Three Questions to Ask Before Signing the Application

Before purchasing an annuity, ask the agent: What is the total commission as a percentage of premium? The agent may not volunteer this, but you have a right to know. If the commission is 7% or higher, the surrender charge is likely to be steep.

Second, how many years until the surrender charge reaches zero? If the schedule is 10 years, you should plan to hold the annuity that long. If you might need the money sooner, a shorter surrender period or a product with a free-withdrawal provision (typically 10% of account value per year without penalty) may be better.

Third, what is the market value adjustment formula? Some contracts use an MVA that can increase the surrender loss if interest rates have risen. Ask for an illustration showing the impact of a 1% or 2% rate increase.

Finally, is the agent acting as a fiduciary under the SEC's Regulation Best Interest? This rule requires brokers to act in the client's best interest when recommending annuities, but it does not require them to disclose commissions. Ask directly whether the recommendation is based on a fiduciary standard or a suitability standard.

Real-World Example: The Cost of Early Surrender

Consider a hypothetical buyer named Sarah who purchases a variable annuity with a $200,000 premium. The agent receives a 7% commission ($14,000) in year one. The surrender charge starts at 11% and declines by 1% each year. If Sarah needs to withdraw the full account value in year two due to an emergency, she faces an 11% surrender charge on the amount withdrawn above the free-withdrawal allowance (typically 10% of account value). Assuming no growth, her account value is $200,000. She can withdraw 10% ($20,000) without penalty, but the remaining $180,000 is subject to an 11% charge of $19,800. Combined with the 10% early withdrawal penalty on gains (if any), the total cost could exceed $20,000. This example illustrates how the surrender schedule can create a significant financial barrier to accessing funds.

Trade-Offs: Surrender Schedule vs. Other Investment Liquidity

Annuities are often compared to other long-term investments like mutual funds or ETFs. A typical mutual fund has no surrender charge; you can sell shares at any time and receive the net asset value. However, mutual funds may impose short-term redemption fees (e.g., 1–2% if sold within 90 days) and are subject to market volatility. Annuities offer principal protection in fixed products and tax deferral, but at the cost of illiquidity. For example, a $100,000 investment in a bond fund may lose value if interest rates rise, but you can sell immediately. In contrast, a fixed annuity guarantees principal but locks you in for 7–10 years. The trade-off is between liquidity and guarantees. Investors who prioritize access to cash should favor products with shorter surrender periods or no surrender charges, such as no-load annuities or immediate annuities (which offer income but no lump-sum access).

Counter-Argument: Are Surrender Charges Unfair?

Critics argue that surrender charges are opaque and disproportionately penalize buyers who face unexpected financial needs. Consumer advocates note that the average annuity buyer is over age 60, and many have limited financial literacy. A 2023 study by the Consumer Financial Protection Bureau found that older investors are more likely to be sold high-commission annuities with long surrender periods. On the other hand, insurers defend surrender charges as necessary to cover acquisition costs and offer guarantees. Without them, they argue, commissions would be lower, and agents would have less incentive to sell annuities, reducing consumer access to guaranteed income products. The debate centers on whether the benefits of annuities justify the lock-in. For buyers who hold to maturity, the surrender charge is a non-issue; for those who surrender early, it can be a severe penalty. The key is informed consent: buyers should understand the schedule before purchasing.

Data Point: How Surrender Charges Affect Persistency

Industry data from LIMRA (2024) shows that surrender rates for deferred annuities are highest in years 2–4, when the penalty is still steep but some buyers face life events. Approximately 15–20% of deferred annuity contracts are surrendered within the first five years. This suggests that a significant minority of buyers do not hold long enough to benefit from the product. The average surrender charge paid by these early exiters is about 7–8% of account value. Insurers use this revenue to offset the commissions paid on policies that persist. Thus, the surrender schedule functions as a risk-sharing mechanism: buyers who stay subsidize the costs of those who leave early.

For more context on how fees can be hidden, see this analysis of fixed annuity prospectuses. And for a look at how tax rules affect trust distributions, see this article on GST-exempt trusts.

This article is for informational purposes only and does not constitute personalized financial, tax, or legal advice. Consult a qualified professional before making any investment decisions.