The Fixed Annuity Prospectus That Hides the 4% Cash Surrender Fee

You read the prospectus cover to cover, yet the 4% cash surrender fee still caught you off guard. It is not that the fee is absent—it is that the document buries it in a footnote, on page 37, under a subheading that reads "Surrender Charge." The typical fixed annuity contract imposes a 4% penalty on the entire account value if you withdraw more than the free allowance during the first several years. That 4% applies to your principal, not just the gains. Over a 10-year surrender period, the fee declines by roughly 1% each year, but the early years are the most expensive. This article walks through the mechanics, the tax consequences, and the strategies to minimize or avoid the charge entirely.

The 4% Fee That Vanishes in Fine Print

Standard disclosure language for fixed annuities typically lists surrender charges in a table titled "Contract Charges." But the table often appears after several pages of marketing language about tax deferral and guaranteed growth. The 4% cash surrender fee is a charge on early withdrawals—meaning any money you take out beyond the free withdrawal allowance (commonly 10% per year) during the surrender period. The fee is calculated on the amount withdrawn, not on gains alone. If you have a $100,000 account and withdraw $20,000 in year two, you may owe 4% of $20,000, or $800.

The fee triggers only on early withdrawals. If you hold the annuity until the end of the surrender period—often 7 to 10 years—you pay nothing. But life happens: job loss, medical bills, or a better investment opportunity. The prospectus footnote 14, buried in the fine print, reveals that the surrender charge is deducted from the account value before the proceeds are sent to you. That means the fee reduces your net cash, and you cannot negotiate it away after the contract is issued.

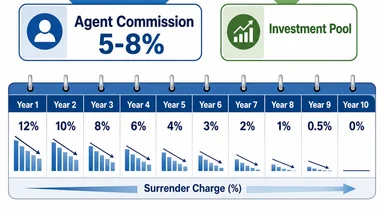

The average surrender period for fixed annuities sold through agents is around 7 years. Some contracts have a declining scale: 4% in year one, 3% in year two, down to 0% after year seven. But the starting percentage can vary. Some carriers charge 5% or 6% in the first year. The key is to check the prospectus's fee table for the exact schedule. Do not rely on the agent's summary—read the actual document.

Why bury the fee? Insurance companies argue that the surrender charge compensates them for upfront commissions and administrative costs. But from the consumer's perspective, it is a penalty for changing your mind. The fee is not illegal, but it is often poorly understood. A 2024 study by the Insured Retirement Institute found that roughly 40% of annuity owners did not know their contract had a surrender charge. That is a lot of people paying a fee they did not expect.

How Surrender Fees Are Calculated and Collected

The surrender fee is calculated as a percentage of the amount withdrawn that exceeds the free withdrawal allowance. Most fixed annuities allow you to take out up to 10% of the account value each contract year without penalty. If your account is worth $100,000, you could withdraw up to $10,000 in year one with no charge. But any amount above that triggers the applicable surrender percentage. For example, if you withdraw $15,000, the excess $5,000 is subject to the 4% fee, costing you $200.

The fee declines by 1% each contract year in many contracts. A typical schedule: year 1: 4%, year 2: 3%, year 3: 2%, year 4: 1%, year 5 and later: 0%. But some carriers use a flat 4% for the first four years, then drop to 0% in year five. Always check the exact schedule in your prospectus. The carrier deducts the fee from the account value when you process the withdrawal. You receive the net amount. If the fee is $800, your account balance is reduced by that amount, and the remaining funds continue to grow tax-deferred.

Partial withdrawals may also incur the charge if they exceed the free allowance. Some contracts allow multiple free withdrawals per year, but others limit it to one. Read the free withdrawal provision carefully. If you take a full surrender, the entire account value (minus any free allowance you have already used) is subject to the fee. That can be a shock if you need all your money at once.

Some annuities include a market value adjustment (MVA) on top of the surrender fee. The MVA adjusts the cash value based on interest rate changes since the contract was issued. If rates have risen, the MVA can reduce your payout further. The MVA is separate from the surrender charge and is disclosed in a different section of the prospectus. Together, these charges can eat up a significant portion of your savings.

Comparing Fixed Annuity Fees to Other Products

Fixed annuities are not the only product with early withdrawal penalties. Certificates of deposit (CDs) often charge a penalty of six months' interest for early withdrawal. On a 5-year CD earning 4%, that penalty might be 2% of principal—less than a typical annuity surrender fee. But CDs do not offer tax deferral, and the penalty is capped at a few months' interest, not a percentage of the entire account.

Variable annuities add another layer: mortality and expense (M&E) charges, typically around 1.25% per year. These fees are ongoing, not just on withdrawal. Indexed annuities cap returns but still have surrender fees similar to fixed annuities. The no-load deferred annuity is an alternative with zero surrender fee, but these are less commonly sold because agents earn no commission. You usually buy them directly from the carrier.

Mutual funds have 12b-1 fees hidden in the expense ratio, but there is no explicit surrender charge. You can sell your shares at any time and pay only capital gains tax. The trade-off is that mutual funds lack the principal guarantee that fixed annuities offer. For someone who values stability and tax deferral, the annuity's surrender fee is a cost of that guarantee.

Some financial planners argue that the surrender fee is a fair trade for the insurance company's risk. But if you are comparing products, look at the total cost over your expected holding period. A CD might have a lower penalty but no tax deferral. A no-load annuity has no surrender fee but may have higher ongoing expenses. There is no perfect product—only the one that fits your situation.

Tax Consequences of Surrendering Early

When you surrender a fixed annuity, any gains are taxed as ordinary income. That is different from capital gains rates on stocks held over a year. If you are in the 22% tax bracket, your annuity gains are taxed at that rate. On top of that, if you are under age 59½, the IRS imposes a 10% early withdrawal penalty on the gain portion. That penalty applies to the taxable amount, not the entire withdrawal. So if you surrender a $100,000 annuity with $20,000 of gain, you owe tax on $20,000 plus a $2,000 penalty.

The tax hit compounds the financial sting of the surrender fee. If you pay a 4% surrender fee on the full $100,000, that is $4,000. Add tax and penalty on the gain, and your net proceeds could be substantially less than your original investment. That is why advisors often warn against buying an annuity with money you might need in the near future.

A 1035 exchange allows you to move your annuity to another contract without triggering immediate tax. You can exchange into a lower-fee annuity or a different product type, as long as it is also an insurance contract. The exchange defers the tax until you actually withdraw money. But if you surrender the new contract early, you may face a new surrender fee. Some annuities have a waiver of surrender charge upon death or nursing home confinement, but those provisions vary.

Partial surrenders are treated as gain first under the tax rules. That means if you take a partial withdrawal, the IRS assumes you are pulling out earnings before principal. So even a small partial surrender can trigger taxable income. The free withdrawal allowance helps avoid this, but any amount beyond the allowance is taxable to the extent of gain. Check your contract's order of withdrawal rules; some annuities allow you to specify that withdrawals come from principal first, but that is rare.

Who Benefits from the Surrender Fee Structure

The surrender fee primarily benefits the insurance company and the agent. Agents earn an upfront commission, typically 5–7% of the premium. That commission is paid by the carrier, which recoups it through surrender fees charged to policyholders who leave early. If you hold the annuity for the full surrender period, the carrier still makes money from the spread between what it earns on investments and what it credits to your account. But the surrender fee reduces the carrier's risk of losing money on clients who lapse early.

The carrier also uses surrender fees to stabilize reserves. Insurance companies invest premiums in long-term bonds and mortgages. If too many policyholders cash out early, the carrier may have to sell assets at a loss. The surrender fee discourages that behavior and helps match assets to liabilities. From the carrier's perspective, it is a risk management tool.

Long-term holders effectively subsidize early leavers. The carrier charges everyone the same spread, but early leavers pay the surrender fee, which covers the carrier's costs. Holders who stay for the full term pay no fee, but the carrier's investment returns may be lower because it had to set aside reserves for potential lapses. Some critics argue that the surrender fee is excessive relative to the actual cost to the carrier. For instance, the Consumer Federation of America has publicly called for standardized fee disclosure and lower surrender charges, highlighting cases where fees exceeded 10% of principal in the first year.

The fee also discourages rate shopping after the contract is issued. If you buy an annuity and interest rates rise, you might want to surrender and buy a higher-rate product. The surrender fee makes that move expensive, locking you into the original contract. That benefits the carrier, which can keep your money at a lower rate. For the consumer, it means you need to be confident in the product before you buy.

Reading the Prospectus for Hidden Charges

Start with the fee table, usually titled "Contract Charges" or "Fee Table." Look for the line labeled "Surrender Charge" or "Contingent Deferred Sales Charge." That line shows the percentage by year. If the table says "4% in year 1," the fee is 4% of the amount withdrawn. Some prospectuses use a different name, like "Withdrawal Charge." Read the footnotes below the table; they often contain exceptions and free withdrawal details.

Check the free withdrawal provision. Most contracts allow 10% of the account value per year without charge, but some allow 10% of premiums paid, or a flat dollar amount. The provision may also specify whether unused free withdrawals carry over to the next year. Many do not. If you skip a year, you lose that allowance. Also note that the free withdrawal may not apply to gains if the contract uses a gain-first tax rule.

Look for a market value adjustment (MVA) clause. The MVA is separate from the surrender fee and applies when interest rates change. If rates rise, the MVA reduces your cash value. The prospectus should describe how the MVA is calculated, often using a formula based on Treasury yields. Some annuities have no MVA; they are called "book value" annuities. Those are simpler but may have a lower credited rate.

Rider fees can stack on top of the base contract. Common riders include a guaranteed minimum income benefit (GMIB) or a death benefit. Each rider has an annual fee, typically 0.5% to 1% of the account value. These fees are deducted from the account annually. If you surrender, you lose the rider benefits, but you still paid the fees. Ask for a "hypothetical surrender value" illustration that shows the net cash value after all fees and taxes at each year. Many carriers will provide one upon request.

Strategies to Avoid or Minimize the Fee

The simplest strategy is to hold the annuity beyond the surrender period. If you can wait until year seven, the fee drops to zero. That means choosing an annuity with a surrender period that matches your time horizon. If you think you might need the money in five years, do not buy a seven-year surrender period. Some carriers offer annuities with shorter surrender periods, such as three or five years, though the credited rate may be lower.

Use the free withdrawal allowance annually. If your contract allows 10% per year, take that amount each year to reduce your exposure. You can reinvest the money in a different account or use it for expenses. Over several years, you can move a significant portion of your funds without paying a surrender fee. But remember that partial withdrawals may be taxable if they exceed your basis. These are general strategies; always consult a financial professional for advice tailored to your situation.

Consider a no-surrender-charge annuity. These products have no surrender fee, but they often have lower credited rates or higher ongoing expenses. They are sold mainly through fee-only advisors or directly from carriers. The trade-off is that you give up some potential growth for liquidity. For someone who values flexibility, the lower return may be acceptable.

Use a 1035 exchange to move into a lower-fee contract. If your current annuity has a high surrender fee, you can exchange it for a different annuity with a lower fee or no surrender charge. The exchange defers tax, but you may face a new surrender period. Some carriers offer exchange programs with reduced surrender charges for incoming transfers. Compare the costs of staying versus moving over your expected holding period.

Ladder annuities to stagger surrender dates. Instead of putting all your money into one annuity, buy several smaller contracts with different surrender periods. For example, one with a 3-year, one with a 5-year, and one with a 7-year surrender period. As each contract matures, you can decide whether to renew or withdraw without penalty. This strategy provides liquidity and reduces the risk of needing to surrender a large contract early. Again, these are general concepts; consult a professional to see if laddering fits your goals.

Conclusion: Balancing Flexibility and Guarantees

Fixed annuities offer principal protection and tax deferral, but the surrender fee is a real cost that can catch investors off guard. The key is to understand the fee structure before signing the contract, and to choose a product that aligns with your time horizon. No strategy eliminates all risk: holding to maturity avoids the fee but ties up your money, while no-surrender annuities may offer lower returns. By reading the prospectus carefully, using free withdrawals, and considering laddering or exchanges, you can manage the fee's impact. Ultimately, the best approach depends on your individual financial situation and goals. As with any financial product, thorough research and professional guidance are essential.

Disclaimer: This article is for informational purposes only and does not constitute personalized financial or legal advice. Consult a qualified professional before making decisions about annuity contracts or any financial product.